Why Insurers Prefer Generic Drug Lists: How Formularies Control Costs and Shape Your Prescriptions

Jan, 14 2026

Jan, 14 2026

When you pick up a prescription, you might not think about why your insurer approved one drug but not another-even if they work the same way. The reason? Preferred generic lists. These aren’t random choices. They’re carefully built systems insurers use to save money, and they directly impact what you pay at the pharmacy counter.

What Are Preferred Generic Lists?

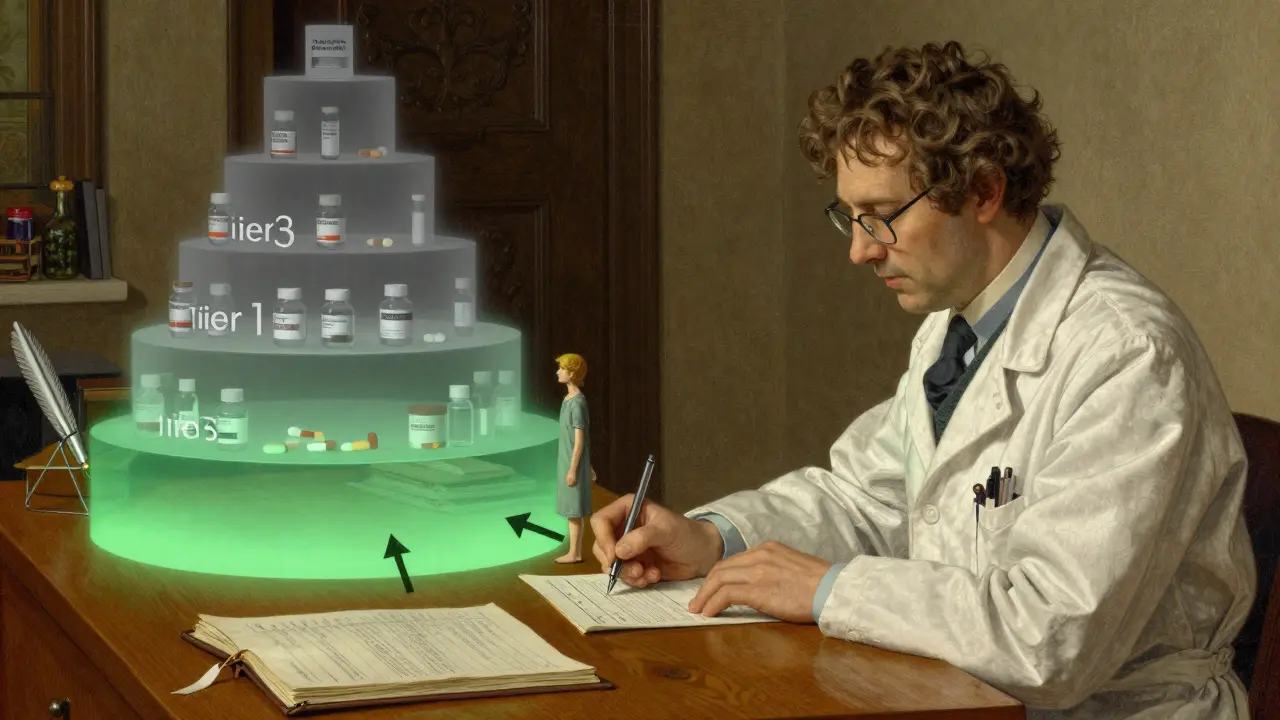

Preferred generic lists, also called formularies, are tiered catalogs of medications that insurance plans approve for coverage. At the bottom of the list-Tier 1-are generic drugs. These are chemically identical to brand-name pills but cost 80-85% less, according to the FDA. Insurers push these first because they work just as well and cost a fraction of the price. For example, levothyroxine, a common thyroid medication, might cost $187 a month as a brand name. As a generic? $12. That’s not a typo. And that’s exactly why insurers want you on the generic version. These lists aren’t just about saving money. They’re designed to guide doctors and patients toward the most cost-effective options without sacrificing safety. Every drug on a preferred list has been reviewed by panels of doctors and pharmacists who check for effectiveness, side effects, and real-world performance. The FDA requires generics to match brand drugs within 80-125% of their bioavailability-meaning they behave the same way in your body. Studies show 98.5% of approved generics meet this standard.How Formularies Are Structured

Most insurance plans use a tiered system, usually with three to five levels. Here’s how it breaks down:- Tier 1: Preferred Generics - These are the cheapest. Copays are typically $5-$15 for a 30-day supply. Think metformin for diabetes, lisinopril for high blood pressure, or atorvastatin for cholesterol.

- Tier 2: Preferred Brands and Some Generics - These are slightly more expensive. Copays range from $25-$50. This tier includes drugs that don’t have a generic yet, or where the generic isn’t preferred for some reason.

- Tier 3: Non-Preferred Brands - These are brand-name drugs with cheaper generics available. Copays jump to $50-$100. Insurers discourage these unless absolutely necessary.

- Tier 4: Specialty Drugs - These are high-cost medications, often biologics like Humira or Enbrel. Copays can be $100+, or you might pay a percentage (like 30%) of the total cost.

Why Insurers Push Generics So Hard

It’s simple math. In 2023, generics made up 90% of all prescriptions filled in the U.S.-but only 23% of total drug spending. That’s a massive gap. When a drug has six or more generic competitors, prices can drop by up to 95%, according to FDA data. Pharmacy Benefit Managers (PBMs)-the middlemen between insurers and drugmakers-negotiate deep discounts on generics. They buy in bulk, often directly from manufacturers, and pass those savings along. In contrast, brand-name drugs rely on rebates, which are less predictable. PBMs get 25-30% rebates on brand drugs, but with generics, they get lower list prices upfront. The savings add up fast. A 2022 study found that patients paid an average of $194 less per prescription when using generics instead of brands-especially when coinsurance (a percentage of the cost) applied. For someone on multiple meds, that’s thousands a year.

Where the System Gets Complicated

Generics work great for most drugs. But not all. Take biologics-complex drugs made from living cells, like those used for rheumatoid arthritis or Crohn’s disease. Biosimilars, the generic versions of biologics, are cheaper. But here’s the catch: brand-name manufacturers often offer co-pay cards that cut your out-of-pocket cost to $0. Biosimilar makers rarely do. So even if a biosimilar costs $850 and the brand costs $1,200, you might still pay more out of pocket with the biosimilar because you lose the manufacturer’s discount. Another issue: drugs with narrow therapeutic indexes, like warfarin (a blood thinner). A small change in dosage can be dangerous. About 23% of doctors resist switching patients to generics here, even if they’re approved. Some patients report feeling different on a new generic-even if labs show the same blood levels. Insurers don’t always account for that. And then there’s step therapy. Many plans require you to try and fail on the preferred generic before they’ll cover the brand. A 2022 AMA report found 42% of physicians saw delays in treating chronic pain because of this rule. One patient might need a brand drug right away due to allergies or side effects-but the system forces them to waste weeks trying cheaper options first.What You Can Do About It

You don’t have to accept whatever your insurer says. Here’s how to take control:- Check your formulary before enrolling. During open enrollment, review your plan’s drug list. If you’re on a medication, make sure it’s on Tier 1. If not, consider switching plans.

- Ask your pharmacist. In 89% of states, pharmacists can swap a brand for a generic unless your doctor writes “dispense as written.” Many patients don’t know this. Ask.

- Appeal if denied. If your drug is denied, your doctor can submit a prior authorization request. In 68% of cases, these appeals succeed when backed by medical evidence.

- Use GoodRx or SingleCare. Sometimes, the cash price for a generic is lower than your insurance copay. Compare prices before paying.

The Bigger Picture

Insurers aren’t being cruel. They’re responding to a broken system. The U.S. spends more on drugs than any other country. Generics are the most effective tool we have to bring that down. But the system is changing. Starting in 2025, Medicare will require biosimilars to be placed in the same tier as their brand-name counterparts. That’s a big deal-it could push biosimilar use from 15% to 45%. At the same time, new rules are forcing insurers to be more transparent about how they decide which drugs go where. Still, challenges remain. Some PBMs now use “accumulator adjuster” programs, which don’t count your biosimilar payments toward your out-of-pocket maximum. That means you could hit your cap faster with a brand drug, even if the generic is cheaper. It’s a loophole that hurts patients. The future? Formularies may shift from price-based tiers to outcome-based ones. Instead of just asking, “Which is cheapest?” insurers might ask, “Which drug keeps patients out of the hospital?” That’s already happening in pilot programs by UnitedHealthcare and others.Real Stories, Real Savings

On Reddit, users share their experiences:- One person switched from brand-name levothyroxine to generic and cut their monthly cost from $187 to $12.

- Another paid $1,200 for Humira, then switched to Amjevita (a biosimilar) and paid $850-only to realize their co-pay card no longer applied, so their out-of-pocket didn’t drop as much as expected.

Final Thoughts

Preferred generic lists aren’t perfect. But they’re the most powerful tool we have to make prescription drugs affordable. They’ve saved the U.S. healthcare system over $1.68 trillion in the last decade. The key isn’t fighting the system. It’s learning it. Know your tiers. Ask questions. Appeal when needed. And don’t assume your doctor’s first choice is the only option. Your health matters. But so does your wallet. The best way to protect both is to understand what’s on your insurer’s list-and why.Why do insurance companies prefer generic drugs?

Insurers prefer generic drugs because they are chemically identical to brand-name drugs but cost 80-85% less on average. This cuts overall drug spending dramatically. For example, a drug with six or more generic competitors can drop in price by up to 95%. Generics help insurers keep premiums lower and reduce out-of-pocket costs for members.

Are generic drugs as effective as brand-name drugs?

Yes. The FDA requires generics to have the same active ingredient, strength, dosage form, and route of administration as the brand-name version. They must also be bioequivalent-meaning they work the same way in the body, within a 80-125% range. Studies show 98.5% of approved generics meet this standard.

What’s the difference between Tier 1 and Tier 3 drugs?

Tier 1 includes preferred generic drugs with the lowest copays-usually $5-$15. Tier 3 includes non-preferred brand-name drugs that have cheaper generic alternatives available. Copays for Tier 3 are much higher, often $50-$100, to encourage patients to choose the generic version instead.

Can I get a brand-name drug if my insurer only covers the generic?

Yes, but you’ll likely pay more. Your doctor can request a prior authorization or exception based on medical necessity-for example, if you had side effects from the generic or if the generic doesn’t work for you. About 68% of these appeals are approved when supported by documentation.

Why are biosimilars harder to switch to than regular generics?

Brand-name biologics often come with co-pay assistance programs that reduce your out-of-pocket cost to $0. Most biosimilar makers don’t offer these. So even if the list price is lower, your actual cost might not drop. Plus, some insurers don’t count biosimilar payments toward your out-of-pocket maximum, making them less financially attractive.

How often should I check my insurance formulary?

You should review your formulary every year during open enrollment. Drug tiers change frequently, and a medication that was covered last year might be moved to a higher tier-or removed entirely. Spending just 45 minutes a year checking your list can save you hundreds or even thousands annually.

Do pharmacists automatically substitute generics?

In 89% of U.S. states, pharmacists can substitute a generic for a brand-name drug unless the doctor writes “dispense as written.” Many patients don’t know this. Always ask your pharmacist if a generic is available and if it’s right for you.

What’s the future of preferred drug lists?

The future is moving from cost-based to value-based formularies. Instead of just choosing the cheapest drug, insurers may start using real-world data-like how often a drug leads to hospital visits-to decide which drugs get preferred status. Medicare’s 2025 rules will push biosimilars into the same tier as brand biologics, and transparency requirements are forcing plans to explain their choices more clearly.

Jaspreet Kaur Chana

January 16, 2026 AT 01:49Man, I never realized how much I was getting ripped off until I switched my thyroid med to generic. Went from $187 to $12 a month - that’s not savings, that’s a heist reversal. In India, we don’t even have brand-name options for most stuff, so we’re used to generics, but seeing how the US system works? Wild. I’ve seen friends here pay hundreds for meds that cost less than a chai latte in Delhi. Insurers aren’t evil - they’re just playing a rigged game, and we’re the pawns. But hey, knowledge is power. If you know your tiers, you can outsmart the system. I tell everyone I meet: check your formulary like it’s your Netflix subscription. You wouldn’t pay for a show you’re not watching, right?

Haley Graves

January 16, 2026 AT 12:30Stop letting insurers dictate your health. If your doctor says you need the brand, fight for it. Prior authorization isn’t a formality - it’s your right. I’ve helped three family members appeal denials, and all got approved with a single letter from their specialist. No emoticons, no fluff - just facts, dates, and medical records. You don’t need to be loud. You just need to be prepared. And if your pharmacist tries to swap your med without asking? Say no. Write ‘dispense as written’ on the script. It’s legal. It’s simple. And it’s your body.

Frank Geurts

January 17, 2026 AT 18:48It is, indeed, a matter of considerable public interest and systemic importance that pharmaceutical cost-containment mechanisms, such as tiered formularies and preferred generic lists, have been implemented with such widespread efficacy across the United States healthcare infrastructure. The FDA’s bioequivalence standards, which mandate a 80–125% therapeutic equivalence window, are not merely regulatory formalities - they are scientifically rigorous benchmarks that have been validated by over two decades of post-marketing surveillance and clinical outcome studies. Furthermore, the role of Pharmacy Benefit Managers in negotiating volume-based discounts on generic pharmaceuticals has demonstrably reduced aggregate national drug expenditure by over 1.68 trillion dollars since 2013, according to the Congressional Budget Office. It is, therefore, both scientifically and economically indefensible to conflate cost-efficiency with substandard care. The perception that generics are inferior is a relic of marketing-driven misinformation, not empirical evidence.

Moreover, the emergence of biosimilars, despite their current market penetration of only 15%, represents a paradigmatic shift toward value-based pharmaceutical pricing. The upcoming Medicare rule mandating co-tiering of biosimilars with originator biologics, effective January 1, 2025, will likely catalyze a 200% increase in adoption, thereby further reducing out-of-pocket burden for patients with autoimmune and oncologic conditions. The so-called ‘accumulator adjuster’ loophole, while ethically dubious, is not a feature of formulary design per se, but rather a perverse incentive structure created by PBM contracts with manufacturers - a problem requiring legislative intervention, not patient self-blame.

Patients who fail to review their formularies annually are, in effect, surrendering their agency to opaque corporate algorithms. A 45-minute annual audit of drug tiers, as cited in the original post, is not an inconvenience - it is a civic duty in an era of healthcare commodification.

Ayush Pareek

January 18, 2026 AT 19:23I’ve been on a few different meds over the years - blood pressure, diabetes, even a little for anxiety - and honestly, I never noticed any difference between brand and generic. I’ve seen people stress out over it, but the science doesn’t lie. My uncle in Punjab was on a brand-name statin for years until we switched him to generic after moving to the U.S. He saved over $200 a month. No side effects. No weird feelings. Just lower bills. I think the real issue isn’t the drugs - it’s the lack of education. Most people don’t even know what a formulary is. If we taught this in high school health class, we’d save millions. And yeah, step therapy sucks sometimes, but if your doc pushes back with real data, it usually works out. Don’t give up. You’re not alone in this.

Nilesh Khedekar

January 20, 2026 AT 07:30Oh, so now it’s ‘the system’? Hah. Let me guess - the same ‘system’ that lets PBMs pocket 30% rebates on brand drugs while telling you generics are ‘better’? And biosimilars? Sure, they’re cheaper… unless your co-pay card vanishes the moment you switch, and now you’re paying $850 out-of-pocket for something that used to be $0. And don’t even get me started on accumulator adjusters - where your payments DON’T count toward your deductible? That’s not a loophole. That’s fraud. And the FDA’s 98.5% bioequivalence stat? Yeah, that’s true… but what about the 1.5% who feel like crap on generics? Who cares? They’re just ‘anecdotal.’ Meanwhile, my neighbor’s mom had a seizure after switching to a generic warfarin. Her INR was ‘fine’ on paper. But her brain? Not so much. So yeah - ‘know your tiers.’ But also know: this system is rigged to make you feel guilty for needing help.

Jami Reynolds

January 21, 2026 AT 07:38Did you know that the FDA doesn’t test generics for long-term effects? They only test for bioequivalence over 24 hours. What happens after 6 months? What about the 23% of doctors who refuse to switch patients on narrow-therapeutic-index drugs? And why do 63% of patients get hit with prior auth surprises? Because insurers are using AI to predict who’ll appeal - and then denying them preemptively. This isn’t about savings. It’s about control. The ‘formulary’ is a surveillance tool. Every time you’re forced to try a cheaper drug, they’re logging your compliance. Soon, your premiums will be adjusted based on how obedient you are. And don’t tell me about GoodRx - those cash prices? They’re often just the list price before the PBM takes its cut. You’re not saving money. You’re being manipulated.

Amy Ehinger

January 22, 2026 AT 09:51I used to be super stressed about meds - I’m on three, and I’d panic every time my copay changed. Then I started using GoodRx every time I filled a script. Sometimes the cash price was cheaper than my insurance. Crazy, right? I also just started asking my pharmacist, ‘Is there a cheaper version?’ and they always say yes. One time they even called my doctor to see if I could switch. No drama. No yelling. Just a simple question. And yeah, I checked my formulary during open enrollment last year and switched plans because my anxiety med got bumped to Tier 3. I saved $400. It’s not magic. It’s just paying attention. I know it’s annoying, but honestly? It’s like budgeting for groceries. You wouldn’t buy the same brand without checking sales, so why do it with your health? Just… check the list. It’s worth 45 minutes.

RUTH DE OLIVEIRA ALVES

January 24, 2026 AT 02:06The structural integrity of the U.S. pharmaceutical reimbursement model is predicated upon the principle of cost-effectiveness, which, in turn, is operationalized through tiered formularies and evidence-based clinical guidelines. The adoption of preferred generic lists is not a capricious policy decision, but a statistically validated mechanism to mitigate the unsustainable inflation of pharmaceutical expenditures, which have, since 2000, increased at a rate three times that of general inflation. The FDA’s bioequivalence requirements, codified under 21 CFR § 314.94, are not permissive thresholds but stringent pharmacokinetic benchmarks that ensure therapeutic equivalence across the entire patient population. Furthermore, the 98.5% compliance rate observed in post-marketing studies corroborates the clinical safety and efficacy of generic formulations. The concerns regarding biosimilars and accumulator adjusters are valid, yet they represent contractual anomalies - not systemic failures of formulary design. The onus, therefore, rests not upon insurers, but upon patients and providers to engage proactively with formulary documentation, advocate for exceptions when clinically indicated, and leverage available tools such as GoodRx and prior authorization protocols to ensure equitable access. Informed patient agency, not systemic distrust, is the most effective countermeasure to pharmaceutical inequity.